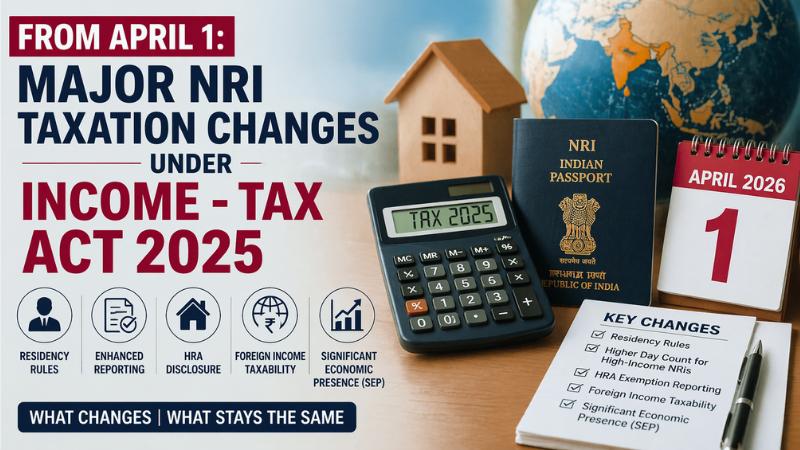

India’s new Income-tax Act, 2025, effective from April 1, 2026, introduces several updates, but for Non-Resident Indians (NRIs), many core rules remain unchanged. The framework continues to maintain the fundamental conditions used to determine an individual’s residential status.

Under the updated law, an individual is still considered a tax resident if they stay in India for 182 days or more in a financial year, or meet the combined condition of 60 days in the current year and 365 days over the previous four years. These basic residency rules remain the same, providing continuity for NRIs. However, a key modification applies to high-income individuals. NRIs earning more than ₹15 lakh in India may now fall under an extended rule where the 60-day condition is replaced with 120 days, making it easier to trigger tax residency in certain cases.

The new Act also introduces enhanced reporting requirements. Taxpayers claiming house rent allowance (HRA) exemptions must now disclose their relationship with the landlord as part of updated compliance rules. This change aims to improve transparency in tax filings.

Another important update relates to foreign income and taxation rules. The Act expands the scope of income that may be considered taxable in India, including income linked to India even if earned abroad, unless covered under tax treaties. Authorities now have more flexibility in determining taxable income using reasonable methods when direct calculations are not possible. New provisions around Significant Economic Presence (SEP) define when a non-resident may be subject to Indian tax, even without a physical presence. This applies when transactions or user engagement in India cross specified thresholds